Africa Unconstrained: Perspectives on the Continent’s New Era challenges current narratives on the economic future of African countries.

We use in-depth analysis, webinars, interviews with global experts and original research to bring out the key economic challenges – and their solutions – for African countries and their partners.

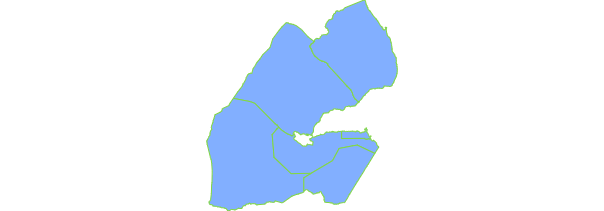

Djibouti’s economy struggled in the 1990s with overall negative growth on average in the period from 1991 to 1999 due to droughts and a civil war. Nevertheless, the country did not qualify for participation in the HIPC initiative as it was judged not to be heavily indebted. There is also no public mention of debt relief from China over the same period.

Djibouti’s public debt remained subdued throughout the 2000’s as the fragile nature of the country meant global creditors are unwilling to extend debt to it.

However, since 2013, external debt has increased fast, peaking at 122% of GDP in 2017, compared to general government debt of only 48%. The discrepancy between these figures is indicative of the private sector and off-balance-sheet state owned enterprises engaging in externally financed infrastructure projects.

5.5%

Economic Growth

1 / 8

DR's Debt Transparency Index

40.3%

Gross Debt Position % Of GDP

-14.6%

Budget balance 2021

Djibouti

Debt to GDP Ratio

Since the 2010s, Djibouti has seen an economic boom due to heavy infrastructure investment as well as rising trade flows, with annual GDP growth averaging 7.1% from 2015 to 2019.[1] There has been a considerable increase in government spending on major construction projects, including a railway line and enhanced port activities in line with Djibouti’s attempts to leverage its strategic position in the Horn of Africa. With most infrastructure in the hands of state-owned enterprises, the country has had to accumulate substantial debt to finance these projects: as of 2018, the public debt to GDP ratio stood at 104%.

Djibouti’s fiscal deficit peaked at 15.4% of GDP in 2015 due to capital expenditure on the two aforementioned large-scale projects, subsequently declining to 0.8% of GDP in 2019 as these projects approached completion. The two projects in question are: (i) a railway network between Djibouti and Addis Ababa to improve trade links (see below) and (ii) five new or expanded ports. This decline in expenditure outweighed the corresponding fall in government revenue attributed to tax exemptions for key activities, including free trade zones. Meanwhile, total debt service as a share of GNI has more than tripled since 2015 to 21.4% by 2019 because LIBOR-indexed interest rates associated with Djibouti’s loan portfolio rose in the late 2010s. Ultimately, in 2019, the IMF assessed Djibouti’s debt situation as being sustainable: despite growing debt, key loans had been restructured, reducing pressure on national debt servicing capacity.

Djibouti scored the joint lowest in this reports’ Debt Transparency Index, with a score of 1, which was awarded for Djibouti’s functioning Debt Management Office, which has previously received EU funding and training. However, in all other aspects of debt transparency, Djibouti scored zero.

Djibouti

Revenue and Budget Balance

No Data Found

China is Djibouti’s largest creditor, with Chinese credit accounting for 58% of the country’s total external debt stock. Equally, 58% of Djibouti’s debt servicing costs are paid to China. Djibouti has used Chinese loans to finance a $3.5 billion free trade zone, expected to be the biggest in the continent, in addition to constructing a railway, two airports and a pipeline. While these projects will no doubt generate new economic growth, some other creditors have expressed concern that Djibouti is too exposed to Chinese debt, which may leave it vulnerable and unable to access financing from them Indeed, whilst the country previously sought financing from the U.A.E., Saudi Arabia, Kuwait, Europe, and Turkey it is no longer the case today.

China Debt : GDP Ratio (%)

External Debt Stock to China vs. Other Countries (USD millions)

No Data Found

The IMF considers Djibouti’s debt to be sustainable under the baseline scenario, but with a high risk of debt distress given any further economic shock, as their ability to service debt could be substantially weakened. Similarly, the Jubilee debt campaign predict a debt crisis in 2020. The IMF and Jubilee believe that debt vulnerability has grown because of a too heavy focus on big investment projects in a few sub-sectors at the expense of holistic efforts to improve factor productivity, debt management and domestic resource mobilization. Multilateral organisations believe this is reinforced by structural challenges in governance.

Nevertheless, these large investment projects are a source of growth, albeit vulnerable to external shocks. The small Djiboutian economy is heavily dependent on port operations: the manufacturing and service sectors revolve almost entirely around the port’s activities, accounting for more than 80% of GDP. Over 80% of the port’s operations in turn involves Ethiopian trade: Ethiopia is Djibouti’s largest trading partner, and as a landlocked nation, relies on access to the Port of Djibouti to transport its goods. Djibouti’s foreign exchange earnings are likely to fall due to lower demand for Ethiopian exports in 2020 on the back of weak global demand and supply chain disruptions. As a result, Djibouti’s heavy reliance on foreign exchange creates potential vulnerabilities in servicing its debt.

External Debt

No Data Found

No Data Found

Acknowledgements:

WRITERS Joe Peissel and Yike Fu GRAPHIC DESIGNER Kayode Animashaun

and The Development Reimagined Team